ATO compliant reports including inspection for tax depreciation schedules and capital gains tax reports

Work with DAVID LEE DEPRECIATION

Property Depreciation, Business Asset Depreciation and Balancing Adjustment Reports

The ATO has provided extensive tax publications and access to tax rulings to me to ensure all my reports comply with current legislation

<!-- Google tag (gtag.js) --><script async src="https://www.googletagmanager.com/gtag/js?id=G-RDG63R5J98"></script><script> window.dataLayer = window.dataLayer || []; function gtag(){dataLayer.push(arguments);} gtag('js', new Date());

gtag('config', 'G-RDG63R5J98');</script>

gtag('config', 'G-RDG63R5J98');</script>

Other Services in Depreciation

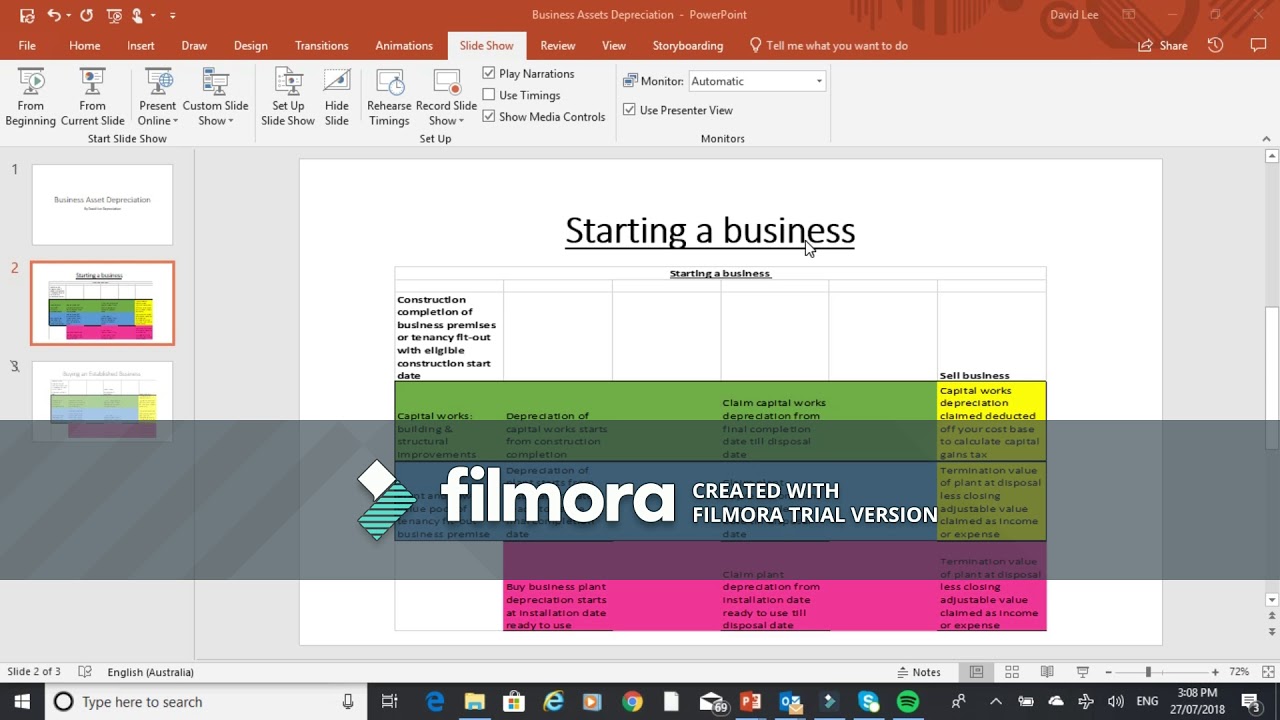

I can also provide balancing adjustment reports for when a property investor or business owner disposes of his/her property or business assets, decides not to hold or use them anymore, or there is an involuntary disposal of the asset.

This involves calculating the difference between the termination value of the asset and its adjustable value at the time of the balancing adjustment event. If there is a balancing adjustment event, a balancing adjustment amount has to be included in your assessable income or claimed as a deduction. Hence, the difference between the termination value and the adjustable value will appear as income or a tax deduction.

If the termination value is greater than the adjustable value, the excess is included in your assessable income. If the termination value is less than the adjustable value, the difference is treated as a deduction.

The termination value is, generally, what you receive or are taken to receive for the asset when the balancing adjustment event occurs. The termination value is made up of amounts you receive and the market value of non-cash benefits such as goods or services you receive for the asset.

Examples of termination values are proceeds from selling an asset or an insurance payout for the loss or destruction of a depreciating asset.

This involves calculating the difference between the termination value of the asset and its adjustable value at the time of the balancing adjustment event. If there is a balancing adjustment event, a balancing adjustment amount has to be included in your assessable income or claimed as a deduction. Hence, the difference between the termination value and the adjustable value will appear as income or a tax deduction.

If the termination value is greater than the adjustable value, the excess is included in your assessable income. If the termination value is less than the adjustable value, the difference is treated as a deduction.

The termination value is, generally, what you receive or are taken to receive for the asset when the balancing adjustment event occurs. The termination value is made up of amounts you receive and the market value of non-cash benefits such as goods or services you receive for the asset.

Examples of termination values are proceeds from selling an asset or an insurance payout for the loss or destruction of a depreciating asset.

As assets that are plant under Division 40 depreciate to values under $1,000, they are eligible to be included in the Low Value Pool as low-value assets, provided the investor/owner has opted to use the Diminishing Value Method.

I can update reports to reflect the movement of plant to the Low Value Pool, where it depreciates faster, giving greater up-front deductions and improving cash flow.

I can update reports to reflect the movement of plant to the Low Value Pool, where it depreciates faster, giving greater up-front deductions and improving cash flow.

When property owners incur capital expenditure on renovations or structural additions to their property I can provide depreciation reports for those capital expenditures.

About David Lee Depreciation

My educational background is in Quantity Surveying from QUT where I achieved first class honors in my bachelor degree

How I Can Help You

If you are a business owner who owns business assets or leases assets with the intention of purchasing them later, you are entitled to depreciation on those assets.

Under income tax law, certain deductions can be claimed for expenditure incurred in producing assessable income, such as carrying on a business. However, the cost of acquiring capital assets is not fully deductible in the year of acquisition. Instead, it must be depreciated as progressive tax deductions over the years of the asset's effective life, as it benefits the business.

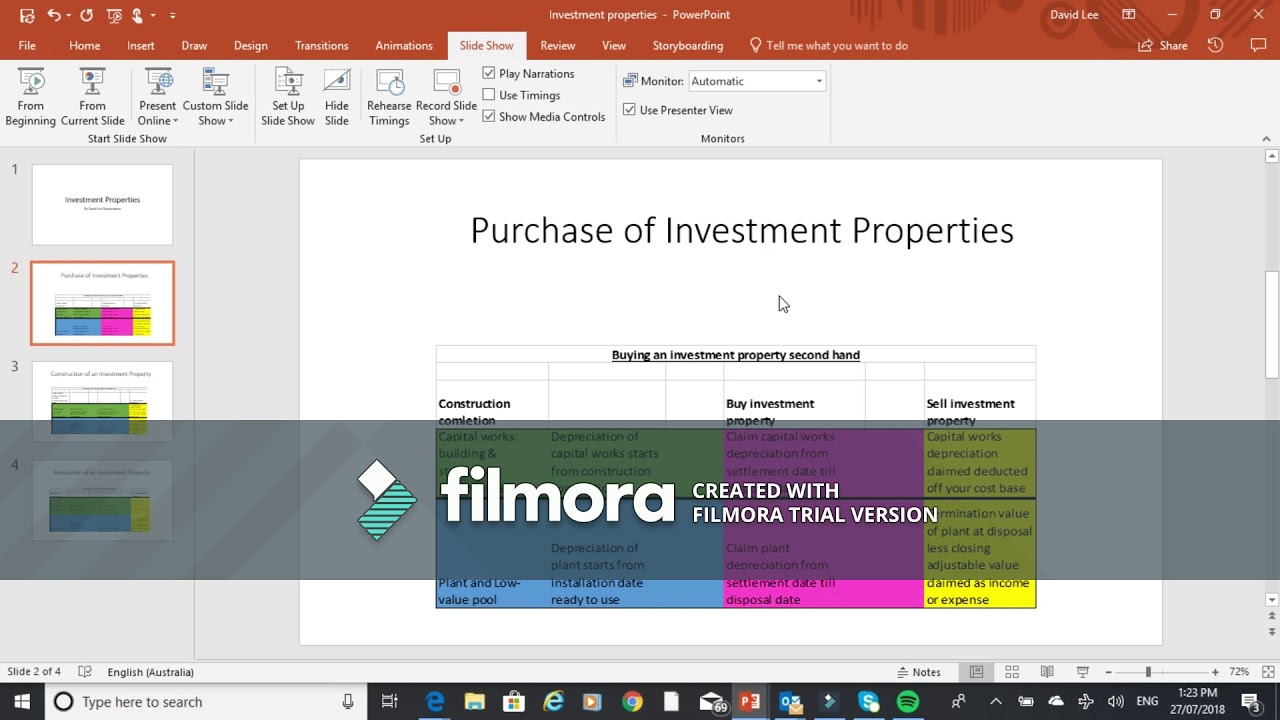

If you own an investment property, you are entitled to depreciation on the plant in the property, as well as any building or structural improvements constructed within eligible dates.

Getting a tax depreciation report done can greatly improve your after-tax cash flow during your ownership of the assets or property. I can help maximize your after-tax cash flow up front and ensure you receive the maximum possible deductions you are entitled to under current ATO legislation.

Under income tax law, certain deductions can be claimed for expenditure incurred in producing assessable income, such as carrying on a business. However, the cost of acquiring capital assets is not fully deductible in the year of acquisition. Instead, it must be depreciated as progressive tax deductions over the years of the asset's effective life, as it benefits the business.

If you own an investment property, you are entitled to depreciation on the plant in the property, as well as any building or structural improvements constructed within eligible dates.

Getting a tax depreciation report done can greatly improve your after-tax cash flow during your ownership of the assets or property. I can help maximize your after-tax cash flow up front and ensure you receive the maximum possible deductions you are entitled to under current ATO legislation.

Purchase your ATO law Compliant Report

Uniform Capital Allowances law states you only claim the plant depreciation for your ownership years as an investment.Order your tax depreciation report now that depreciates all plant from installation date & tabulates the depreciation inherited by you from settlement date.

- Under the new laws in Rental Properties 2018, for contracts signed after 9th May 2017, there is no more depreciation for second-hand plant assets in residential rental properties purchased solely for deriving rental income—unless the property is used for conducting a business, including a rental property business, or you are an excluded entity.

- If you rented out the property after 9th May 2017 but purchased it earlier, then no second-hand assets can be depreciated.

- However, an excluded entity can still claim depreciation on second-hand plant assets in residential properties with contracts signed after 9th May 2017. The excluded entities are:

- A corporate tax entity

- A superannuation plan that is not an SMSF

- A public unit trust

- A managed investment trust

- A unit trust or partnership

.jpeg "Audit")

About

Business owners and property investors who purchase assets or lease assets to purchase later can deduct their depreciation off their taxable income.each plant asset depreciates from its installation date and its cost includes bringing the plant to its condition and location.

Blog: News

if a property is on leased land or a business plant is leased then the lessee is considered to be that assets’ holder and entitled to its depreciation. Each owner of the business or property depreciates their cost of interest in the Plant & capital works.

Services

Plant and Low Value Pool assets depreciate from installation date ready to use and any subsequent buyer of the business plant asset or investment property plant asset inherits the remaining depreciation of that plant asset from settlement of the purchase.

Blog: Natural Disaster Damage Claims

An item of capital equipment which is re-built or replaced is depreciable over an effective life. an improvement to an asset which increases its income generation is also depreciated & not an expense. an insurance payout for these repairs is considered assessable income.