)

About Us

Depreciating assets covered under uniform capital allowances include:

- PLANT

- SOFtWARE

- Mining & quarrying

- Intellectual property

- FORESTRY ROADS & TIMBER MILL BUILDINGS AND SPECTRUM LICENCES

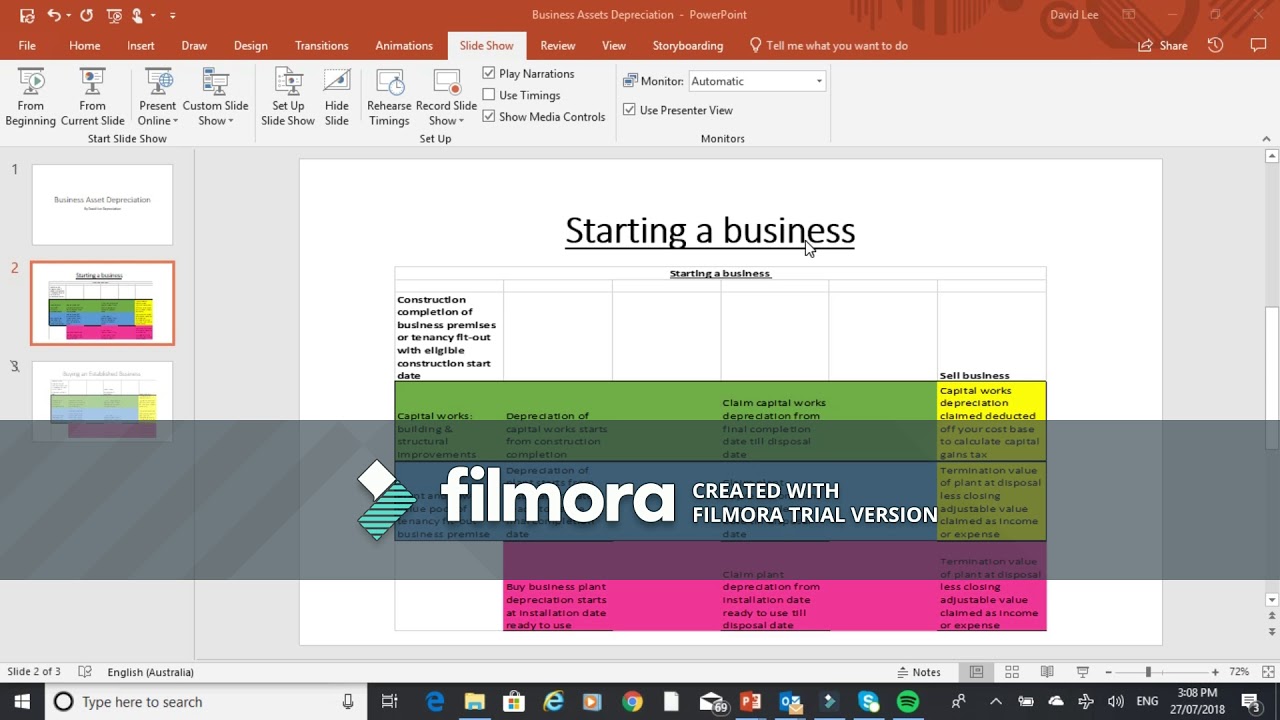

- Any capital works in the tenancy fitout owned by the business is also a depreciating asset and is claimed under Division 43 ITAA.

Business owners and property investors

who purchase assets or lease assets to purchase later can deduct their depreciation off their taxable income. each plant asset depreciates from its installation date and its cost includes bringing the plant to its condition and location.

For reports with both 40 year Diminishing Value & 40 year Prime Cost taxflow

Plant and Low Value Pool assets

depreciate from installation date ready to use and any subsequent buyer of the business plant asset or investment property plant asset inherits the remaining depreciation of that plant asset from settlement of the purchase.

After damage from natural disaster repairs of capital items can be treated as an expense that fy but replacement of capital items must be depreciated over the plant’s effective life

An item of capital equipment

which is re-built or replaced is depreciable over an effective life. an improvement to an asset which increases its income generation is also depreciated & not an expense. an insurance payout for these repairs is considered assessable income.

Business Plant Assets when disposed are treated as income/loss in that financial year

Many business plant assets are disposed of for nominal amounts that can be deducted off remaining depreciation left undeducted for the holder of that plant. This balancing adjustment amount is treated as an expense deduction that fy.

Business Asset depreciation

if a property is on leased land or a business plant is leased then the lessee is considered to be that assets’ holder and entitled to its depreciation. Each owner of the business or property depreciates their cost of interest in the Plant & capital works

Business’s who lease plant are entitled to claim depreciation on that leased asset providing they buy it at the end of the lease. To get depreciation reports on business leased assets including leased vehicles