Services

Business owners and property investors

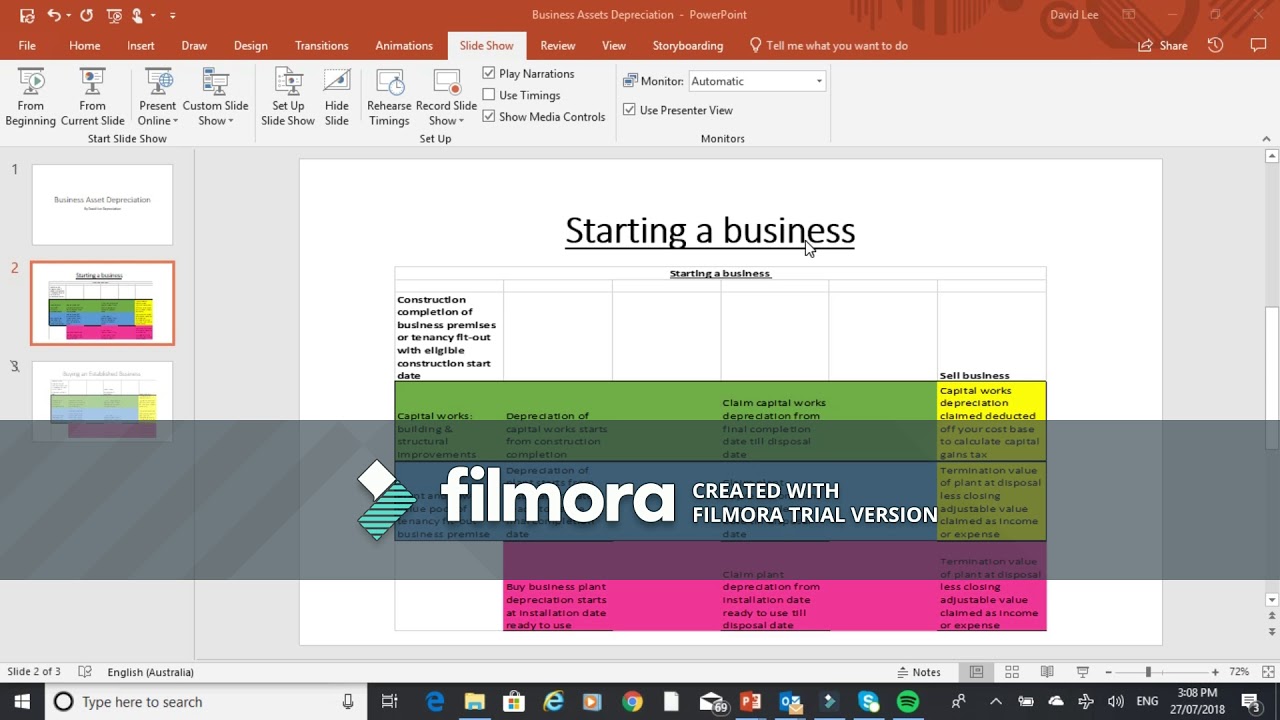

who purchase assets or lease assets to purchase later can deduct their depreciation off their taxable income. each plant asset depreciates from its installation date and its cost includes bringing the plant to its condition and location.

For all plant depreciated from installation date and depreciation tabulated for new owner from settlement date

Plant and Low Value Pool assets

depreciate from installation date ready to use and any subsequent buyer of the business plant asset or investment property plant asset inherits the remaining depreciation of that plant asset from settlement of the purchase.

We do every report using the latest effective lives for plant as determined by the ATO. To see eligible plant lists as provided by the ATO and their latest effective lives see this link to taxation ruling TR 2018/4

An item of capital equipment

which is re-built or replaced is depreciable over an effective life. an improvement to an asset which increases its income generation is also depreciated & not an expense. an insurance payout for these repairs is considered assessable income.

For all reports on investment properties including a full inspection of the property

Business Asset depreciation

if a property is on leased land or a business plant is leased then the lessee is considered to be that assets’ holder and entitled to its depreciation. Each owner of the business or property depreciates their cost of interest in the Plant & capital works